Why Don’t More People Have Life Insurance Coverage?

Ever wondered why more people don’t have life insurance coverage? Our video explores common reasons behind the lack of life insurance, including misconceptions, cost concerns, and lack of awareness. We discuss the barriers to obtaining coverage and offer insights into overcoming these challenges to secure the financial protection you and your loved ones need.

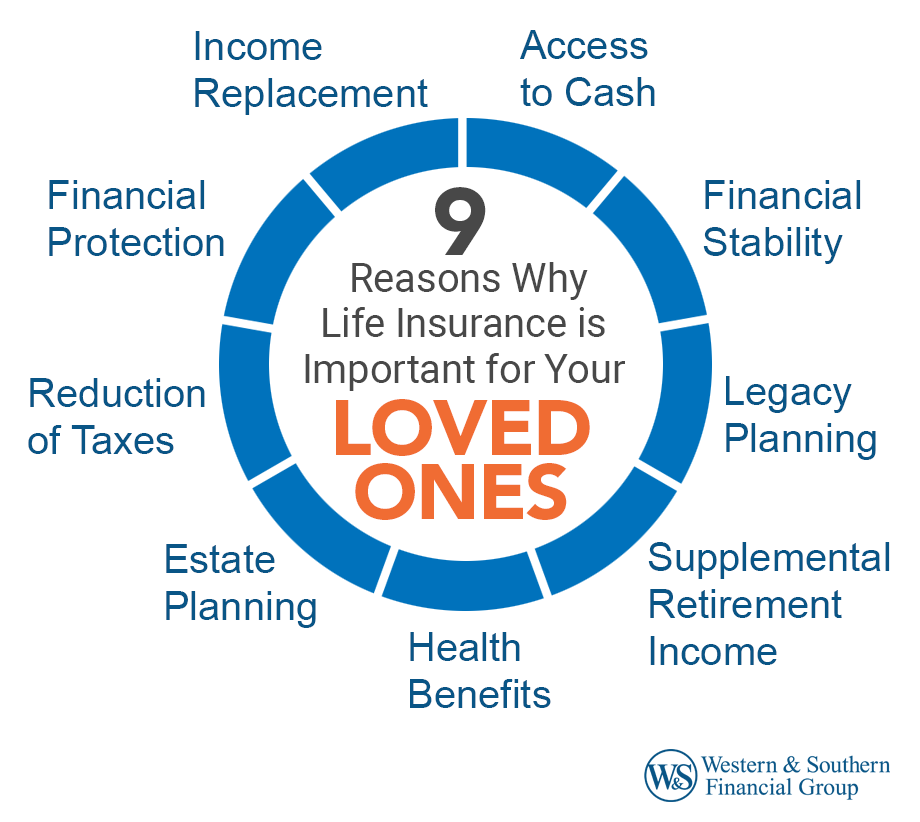

Life insurance is a vital financial tool that offers peace of mind and security for individuals and their families. Despite its importance, a significant portion of the population remains uninsured or underinsured. Understanding the reasons behind this trend can provide insight into the barriers to life insurance coverage and highlight potential solutions to encourage more people to secure their financial futures.

Perceptions of Life Insurance

One of the primary reasons many individuals forgo life insurance is a lack of understanding about its importance and benefits. Many people perceive life insurance as an unnecessary expense, especially if they believe they are in good health or have no dependents. The misconception that only those with significant financial responsibilities need life insurance can lead to an overall underestimation of its value.

Furthermore, some individuals believe that life insurance is primarily for older adults or those with families. This misconception can prevent younger individuals from considering life insurance as a viable option, leading them to miss out on the opportunity to secure lower premiums that are often available to younger policyholders.

Financial Constraints

Another significant barrier to obtaining life insurance coverage is financial constraints. Many people view life insurance premiums as an additional expense they cannot afford, particularly in times of economic uncertainty or personal financial strain. The perception that life insurance is costly can deter individuals from seeking coverage, even if it may be more affordable than they assume.

Additionally, individuals may prioritize immediate financial needs over long-term security. With rising costs of living, student debt, and other financial obligations, many people may choose to allocate their resources toward more pressing matters, neglecting the importance of life insurance in their financial planning.

Complexity of Policies

The complexity of life insurance policies can also contribute to the lack of coverage. Many people find the terminology and options surrounding life insurance confusing, leading to feelings of overwhelm. With various types of policies available, including term life, whole life, and universal life insurance, potential policyholders may struggle to understand which option best suits their needs.

This confusion can result in individuals delaying their decision to purchase life insurance or opting out altogether. The insurance industry often fails to communicate the benefits and differences of these policies in straightforward terms, further complicating the decision-making process for potential buyers.

Distrust of Insurance Companies

Distrust in insurance companies can deter individuals from purchasing life insurance. Negative perceptions surrounding the industry, often fueled by stories of denied claims or complicated payout processes, can lead to skepticism. Potential policyholders may fear that they will not receive the support they expect when it comes time to file a claim.

This lack of trust can result in individuals avoiding life insurance altogether, believing that it is not worth the risk. Building a relationship with a reputable insurance agent and understanding the claims process can help alleviate these concerns and foster trust in the system.

Cultural Influences

Cultural attitudes toward life insurance can also play a role in the coverage gap. In some cultures, discussing death and financial planning is taboo, leading to a reluctance to engage in conversations about life insurance. This cultural stigma can prevent individuals from seeking coverage, as they may feel uncomfortable addressing the topic or discussing their mortality.

Additionally, beliefs surrounding financial planning and the role of life insurance can vary across cultures. In some communities, individuals may rely on family support in times of crisis, making life insurance seem unnecessary. Addressing these cultural perceptions and promoting open discussions about financial security can encourage more people to consider life insurance.

Misunderstanding the Role of Life Insurance

Many individuals misunderstand the purpose of life insurance, often viewing it solely as a means to cover funeral expenses. While this is one aspect of life insurance, its broader purpose is to provide financial protection for dependents and loved ones. This misunderstanding can lead to individuals underestimating the amount of coverage they need or believing that they do not require life insurance at all.

Life insurance is an essential component of a comprehensive financial plan. It can cover various expenses, such as mortgage payments, education costs for children, and other financial obligations. By understanding the full scope of life insurance benefits, individuals may be more inclined to seek coverage.

The Impact of Technology and Online Resources

The rise of technology and online resources has transformed the way people approach life insurance. While these resources can provide valuable information and make the process more accessible, they can also contribute to confusion. The vast amount of information available online can overwhelm potential policyholders, making it challenging to discern trustworthy sources and reliable information.

Additionally, individuals may rely solely on online calculators and comparison tools, which can provide a false sense of security. Without proper guidance from knowledgeable professionals, potential policyholders may struggle to assess their actual needs and choose the right coverage.

Lack of Awareness of Options

Many individuals are simply unaware of the various life insurance options available to them. This lack of awareness can stem from limited exposure to insurance discussions in their personal lives or the media. Without proper education about the different types of policies and coverage options, potential policyholders may feel lost when trying to navigate the market.

Educational initiatives and community outreach can help address this issue. By providing information about the different types of life insurance and the benefits of each, organizations can empower individuals to make informed decisions regarding their financial security.

Negative Experiences with Insurance

Previous negative experiences with insurance, whether personal or witnessed through friends and family, can create a reluctance to engage with life insurance providers. Individuals who have experienced complicated claims processes or perceived lack of support may develop a negative perception of the industry, leading to avoidance of life insurance altogether.

Building positive experiences with insurance companies can help overcome these barriers. Ensuring transparency in the claims process and offering excellent customer service can help foster trust and encourage individuals to seek coverage.

Addressing the Knowledge Gap

Addressing the knowledge gap regarding life insurance is crucial in increasing coverage rates. Many individuals lack basic knowledge about the importance of life insurance and how it fits into their overall financial plan. Educational campaigns and workshops can help demystify the process and provide individuals with the information they need to make informed decisions.

By creating accessible resources and engaging discussions about life insurance, individuals can gain a better understanding of its benefits and relevance in their lives. Encouraging financial literacy and awareness can empower individuals to take charge of their financial futures and consider life insurance as a necessary investment.

Promoting Open Conversations

Encouraging open conversations about life insurance can help combat the stigma associated with discussing death and financial planning. By fostering an environment where individuals feel comfortable discussing these topics, families and communities can normalize the conversation around life insurance.

This openness can lead to increased awareness and understanding of the benefits of life insurance, prompting individuals to consider securing coverage for themselves and their loved ones. Additionally, discussions about financial planning can help individuals recognize the importance of life insurance in protecting their family’s financial well-being.

The Role of Insurance Agents

Insurance agents play a critical role in promoting life insurance coverage. They serve as trusted advisors who can guide individuals through the process of selecting the right policy for their needs. By providing personalized support and education, insurance agents can help demystify the complexities of life insurance.

Encouraging individuals to seek advice from knowledgeable agents can empower them to make informed decisions regarding their coverage. Agents can help potential policyholders assess their needs, explain the different types of policies, and clarify any confusion surrounding the insurance process.

The lack of life insurance coverage among individuals can be attributed to a combination of perceptions, financial constraints, complexity, and cultural influences. By addressing these barriers and promoting awareness, understanding, and open conversations about life insurance, we can encourage more individuals to secure their financial futures. Life insurance is not just a safety net; it is an essential part of financial planning that protects loved ones and ensures peace of mind. With the right resources and support, more people can be empowered to make informed decisions and take advantage of the benefits that life insurance provides.

FAQs

Why do people often think life insurance is unnecessary?

Many individuals perceive life insurance as an unnecessary expense, especially if they believe they are in good health or do not have dependents. This perception can lead to an underestimation of its importance.

How can financial constraints impact life insurance coverage?

Financial constraints can deter individuals from seeking life insurance coverage, as many view premiums as an additional expense they cannot afford, particularly during times of economic uncertainty.

What are some common misconceptions about life insurance?

Common misconceptions include the belief that life insurance is only for older adults, that it is solely meant to cover funeral expenses, and that it is too complex to understand.

How can technology impact the decision to purchase life insurance?

While technology provides access to information about life insurance, the overwhelming amount of resources can also lead to confusion and misinformation, making it difficult for individuals to make informed choices.

What role do insurance agents play in increasing life insurance coverage?

Insurance agents serve as trusted advisors who can guide individuals through the complexities of life insurance, helping them assess their needs and choose the right policy for their situation.

What's Your Reaction?